Paul Samuelson

Paul Anthony Samuelson (May 15, 1915 – December 13, 2009) was an American economist. He was the first American to win the Nobel Prize in Economics.

Quotes

[edit]1940s

[edit]- The General Theory caught most economists under the age of 35 with the unexpected virulence of a disease first attacking and decimating an isolated tribe of south sea islanders. Economists beyond 50 turned out to be quite immune to the ailment. With time, most economists in between began to run the fever, often without knowing or admitting their condition.

- "Lord Keynes and the General Theory", Econometrica (1946)

- Herein lies the secret of the General Theory. It is a badly written book, poorly organized; any layman who, beguiled by the author's previous reputation. bought the book was cheated of his five shillings. It is not well suited for classroom use. It is arrogant, bad-tempered. polemical, and not overly generous in its acknowledgments. It abounds in mares' nests or confusions. In it the Keynesian system stands out indistinctly, as if the author were hardly aware of its existence or cognizant of its properties; and certainly he is at his worst when expounding its relations to its predecessors. Flashes of insight and intuition intersperse tedious algebra. An awkward definition suddenly gives way to an unforgettable cadenza. When finally mastered, its analysis is found to be obvious and at the same time new. In short, it is a work of genius.

- "Lord Keynes and the General Theory", Econometrica (1946)

Foundations of Economic Analysis (1947; 1983)

[edit]- Science is not art. Yet, despite the lack of complete identity between art and science, there is much in common among different creative processes.

- Introduction to the Enlarged Edition

- Just as Hegel is said to have understood his philosophy for the first time when he read its French translation, Vilfredo Pareto could have learned what it was he meant exactly to say when he read Bergson's 1938 classic.

- Introduction to the Enlarged Edition

- I was lucky to enter economics in 1932. Analytical economics was poised for its take-off. I faced a lovely vacuum that young economists today can hardly imagine. So much remained to be done. Everything was still in an imperfect state. It was like fishing in a virgin lake: a whopper at every cast, but so many lovely new specimens that the palate never cloyed.

- Introduction to the Enlarged Edition

- The existence of analogies between central features of various theories implies the existence of a general theory which underlies the particular theories and unifies them with respect to those central features. This fundamental principle of generalization by abstraction was enunicated by the eminent American mathematician E. H. Moore more than thirty years ago. It is the purpose of the pages that follow to work out its implication for theoretical and applied economics.

- Ch. 1 : Introduction

- The general method involved may be very simply stated. In cases where the equilibrium values of our variables can be regarded as the solutions of an extremum (maximum or minimum) problem, it is often possible regardless of the number of variables involved to determine unambiguously the qualitative behavior of our solution values in respect to changes of parameters.

- Ch. 2 : The Theory of Maximizing Behavior

- In the preface to the reissue of Risk, Uncertainty and Profit, Frank Knight makes the penetrating observation that under the conditions envisaged above the velocity of circulation would become infinite and so would the price level. This is perhaps an over-dramatic way of saying that nobody would hold money, and it would become a free good to go into the category of shell and other things which once served as money. We should expect too that it would not only pass out of circulation, but it would cease to be used as a conventional numeraire in terms of which prices are expressed. Interest bearing money would emerge. Of course, the above does not happen in real life, precisely because uncertainty, contingency needs, non-synchronization of revenues and outlay, transaction frictions, etc., etc., all are with us. But the abstract special case analyzed above should warn us against the facile assumption that the average levels of the structure of interest rates are determined solely or primarily by these differential factors. At times they are primary, and at other times, such as the twenties in this country, they may not be. As a generalization I should hazard the hypothesis that they are likely to be of great importance in an economy in which there is a “quasi-zero" rate of interest. I think by this hypothesis one can explain many of the anomalies of the United States money market in the thirties.

- Ch. 5 : Theory of Consumer’s Behavior

Economics (1948-)

[edit]

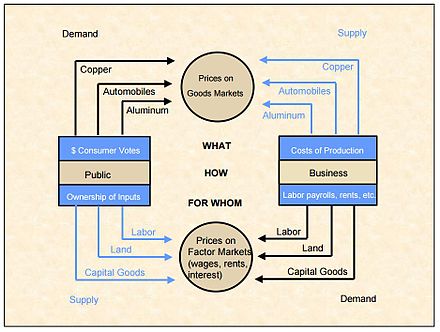

- Figure 12-6 pulls together in a simplified way the main elements of income determination. Without saving and investment, there would be a circular flow of income between business and the public: above, business pays out wages, interest, rents, and profits to the public in return for the services of labor and property; and below, the public pays consumption dollars to business in return for goods and services.

Realistically, we must recognize that the public will wish to save some of its income, as shown at the spigot Z. Hence, businesses cannot expect their consumption sales to be as large as the total of wages, interest, rents, and profits.- 8th ed., 1970, p. 218

1950s

[edit]- I think the acceptance of "mathematical expectation of utility" or its "arithmetic mean" was an unthinking carryover from the mathematical theory of the law of large numbers as applied to asymptotic processes.

- "Probability and the Attempts to Measure Utility", The Economic Review (July 1950)

- Needless to say, the partial equilibrium assumptions involved in the domestic demand schedules and the neglect of aggregative relations constitute a serious defect of such a model except as a rough first approximation to the answers in especially favorable cases. Good economic theory will recognize these limitations rather than be predisposed to neglect them.

- "Spatial Price Equilibrium and Linear Programming", The American Economic Review (June 1952)

- Dynamic process analysis also liberates economists from the necessity of having separate theories of the “turning-points” in addition to theories of cumulative upward and downward swings. Even a simple theory of inventory cycles, or acceleration-multipliers, can explain all four phases of an idealized cycle.

At its best, dynamic analysis can enrich our understanding of possibilities without leading to credulity in new, over-narrow, monistic dogmas concerning the cyclical process.- "Dynamic Process Analysis", in Howard Ellis (ed.), A Survey of Contemporary Economics (1952)

- Econometrics may be defined as the quantitative analysis of actual economic phenomena based on the concurrent development of theory and observation, related by appropriate methods of inference.

- Paul Samuelson, Tjalling Koopmans, and Richard Stone. "Report of the evaluative committee for Econometrica." Econometrica- journal of the Econometric Society. (1954): 141-146.

- Marx did do original work in analyzing patterns of circular inter-dependency among industries. Such work gains few converts and is not very helpful in promoting revolution or counterreactions. But like all pioneering effort it deserves the commendation of later craftmen, and it deserves further development. There is half-truth in Schumpeter's adaption of Clemenceau: "Marxian economics is too hard to be left to the Marxians." Only half, because the present paper is seen to involve little worse than school algebra and to be well within the frontier of modern economic theory.

- "Wage and Interest: A Modern Dissection of Marxian Economic Models", The American Economic Review (December 1957)

- Remember that our goal is not the abolition of all business cycles--even if that were feasible, it might not be desirable. Instead we aim to wopie out persistent slump or unsought inflation. If only capitalism had succeeded in the past in this more modest goal, how different would have been the course of human history!

- "What Economists Know", in Daniel Lerner (ed.), The Human Meaning of the Social Sciences (1959)

- As old problems are conquered, we expect to turn up new problems. A discipline lives on its unsolvved problems; and so, for better or worse, economics is likely to be a lively subject for as many years ahead as man can see.

- "What Economists Know", in Daniel Lerner (ed.), The Human Meaning of the Social Sciences (1959)

1960s

[edit]- Perhaps all we can expect of a public body, charged with grave responsibilities, is that it should in its public utterances make out cases stronger than it really believes in. Or perhaps, because its opposition deals in overly strong criticisms, it may for political reasons and for understandable psychological reasons provide overly strong rebuttals. Or perhaps it is the case that the authorities believe that there are no sensible reasons to doubt the following view: The way to maximize growth, to maximize the long-run degree of achieved employment, to maximize equity among the various social groups that could be affected by price level changes is, in the absence of important cost pressures and even more in their presence, for the Federal Reserve to insist upon the attainment of essentially stable long-run price levels.

- "Reflections on Monetary Policy", The Review of Economics and Statistics, Vol. 42, No. 3 (Aug., 1960)

- In the absence of perfect certainty, the futures prices needed for making the requisite wealth-like comparisons are simply unavailable. So it would be difficult to make operational the theorist’s desired measures. But operational practicality aside, if the theorist specifies in detail the dynamic technology of his model, he will meet none of the pitfalls that come from an attempt to summarize his model by various crude aggregations. The contradictions that result from over-crude aggregation should never be confused with the technical relations that hold at the firm and family level or with the market capitalizations which hold in competitive security and asset markets.

- "The Evaluation of 'Social Income': Capital Formation and Wealth", in F. A. Lutz and D. C. Hague (eds.), The Theory of Capital (1961)

- Economic theory is a mistress of even too tempting grace.

- "Problems of The American Economy: An Economist's View", Stamp Memorial Lectures (1962)

- In every actuarial situation of mathematical probability, no matter how large the numbers in the sample, we are left with a finite sample: in the appropriate limit law of probability there will necessarily be left an epsilon of uncertainty even in so-called risk situations.

- "Risk and Uncertainty: A Fallacy of Large Numbers" Scientia (April-May 1963)

- I will tell you a secret. Economists are supposed to be dry-asdust, dismal fellows. This is quite wrong, the reverse of the truth. Scratch a hard-boiled economist of the libertarian persuasion and you find a Don Quixote underneath. No lovesick maiden ever pined for the days of medieval chivalry with such sentimental impracticality as some economists long for the return to a Victorian marketplace that is completely free. Completely free? Well, almost so. There must, of course, be the constable to ensure that voluntary contracts are enforced and to protect the property rights of each molecule which is an island unto itself.

- "Modern Economic Realities and Individualism", The Texas Quarterly (1963)

- And make no mistake about it: Smith was right. Most of the interventions into economic life by the State were then harmful both to prosperity and freedom. What Smith said needed to be said. In fact, much of what Smith said still needs to be said: good intentions by government are not enough; acts do have consequences that had better be taken into account if good is to follow.

- "Modern Economic Realities and Individualism", The Texas Quarterly (1963)

- Complete freedom is not definable once two wills exist in the same interdependent universe. We can sometimes find two situations in which Choice A is more free than Choice B in apparently every respect and at least as good as B in every other relevant sense. In such singular cases I will certainly throw in my lot with the exponents of individualism. But few situations are really of this simple type; and these few are hardly worth talking about, because they will already have been disposed of so easily. In most actual situations we come to a point at which choices between goals must be made: Do you want this kind of freedom and this kind of hunger, or that kind of freedom and that kind of hunger? I use these terms in a quasi-algebraic sense, but actually what is called "f reedom" is really a vector of almost infinite components rather than a one-dimensional thing that can be given a simple ordering.

- "Modern Economic Realities and Individualism", The Texas Quarterly (1963)

- Libertarians fail to realize that the price system is, and ought to be, a method of coercion. Nature is not so bountiful as to give each of us all the goods he desires. We have, by the nature of things, to be coerced out of such an expectation. That is why we have policemen and courts. That is why we charge prices which are high enough relative to limited money, to limit consumption.

- "Modern Economic Realities and Individualism", The Texas Quarterly (1963)

- Before Rousseau, people made the mistake of treating children as merely adults shrunk small. The Bible and Freud go farther and tell us that an adult is merely a child grown large. Man is imperfect, and so is woman. And so is We, Incorporated, who paternalistically put restraints upon ourselves. Not even an individual's perfections are his alone; like his imperfections, they are group-made. We entered a world we never made, and leave one we did not unmake.

- "Modern Economic Realities and Individualism", The Texas Quarterly (1963)

- Carry the notion of the individual to its limit and you get a monstrosity, just as you do if you carry the notion of a group to its limit.

- "Modern Economic Realities and Individualism", The Texas Quarterly (1963)

- The stock market has forecast nine of the last five recessions.

- Samuelson, Paul (September 19, 1966). "Science and Stocks". Newsweek. p. 92.

- For better or worse, the picture album whose pages I have been turning is that of the main stream of international economics. Many of its advances lie in what the historian of science Thomas Kuhn would call 'normal' rather than 'revolutionary' science. It is hard to imagine having had too good an education and too good a research environment. And yet as we grapple with the ever-changing problems of the modern world that are arising in the deliberations of this World Congress, we know we must put aside the pictures and souvenirs of the past, and we must turn a youthful eye out to meet the emerging universe.

- "The Way of an Economist", in Paul A. Samuelson (ed.), International Economic Relations: Proceedings of the Third Congress (1969)

1970s

[edit]- The very name of my subject, economics, suggests economizing or maximizing. But Political Economy has gone a long way beyond home economics. Indeed, it is only in the last third of the century, within my own lifetime as a scholar, that economic theory has had many pretensions to being itself useful to the practical businessman or bureaucrat. I seem to recall that a great economist of the last generation, A. C. Pigou of Cambridge University, once asked the rhetorical question, “Who would ever think of employing an economist to run a brewery?” Well, today, under the guise of operational research and managerial economics, the fanciest of our economic tools are being utilized in enterprises both public and private.

- "Maximum Principles in Analytical Economics," Prize Lecture, Lecture to the memory of Alfred Nobel, December 11, 1970

- With the assistance of mathematics, I can see a property of the ninety-nine dimensional surfaces hidden from the naked eye. If an increase in the price of fertilizer alone always increases the amount the firm buys of caviar, from that fact alone I can predict the answer to the following experiment which I have never seen performed and upon which I have no observations: an increase in the price of caviar alone will increase the amount the firm buys of fertilizer. In thermodynamics such reciprocity or integrability conditions are known as Maxwell Conditions; in economics they are known as Hotelling conditions in honor of Harold Hotelling’s 1932 work.

- "Maximum Principles in Analytical Economics," Prize Lecture, Lecture to the memory of Alfred Nobel, December 11, 1970

- There is really nothing more pathetic than to have an economist or a retired engineer try to force analogies between the concepts of physics and the concepts of economics. How many dreary papers have I had to referee in which the author is looking for something that corresponds to entropy or to one or another form of energy. Nonsensical laws, such as the law of conservation of purchasing power, represent spurious social science imitations of the important physical law of the conservation of energy; and when an economist makes reference to a Heisenberg Principle of indeterminacy in the social world, at best this must be regarded as a figure of speech or a play on words, rather than a valid application of the relations of quantum mechanics.

- "Maximum Principles in Analytical Economics," Prize Lecture, Lecture to the memory of Alfred Nobel, December 11, 1970

- An American economist of two generations ago, H. J. Davenport, who was the best friend Thorstein Veblen ever had (Veblen actually lived for a time in Davenport’s coal cellar) once said: “There is no reason why theoretical economics should be a monopoly of the reactionaries.” All my life I have tried to take this warning to heart, and I dare call it to your favorable attention.

- "Maximum Principles in Analytical Economics," Prize Lecture, Lecture to the memory of Alfred Nobel, December 11, 1970

- I used to joke to Bob Solow that the distance between me and Joan Robinson is less than the distance between Joan Robinson and me. His reply was, “You’ll never convince her of that.” Still one lives in hope.

- letter to Joan Robinson (April 14, 1972) quoted in Marjorie Shepherd Turner, Joan Robinson and the Americans (1989)

- Inside every classical economist is a modem economist trying to get out. In rereading the Wealth of Nation is, it seems to me that with a little midwifery sleight of hand, one can extract from Adam Smith a valuable model that vindicates him from criticisms of Ricardo and Marx and from the general supercilious discounting of Smith as an unoriginal theorist who is logically fuzzy and eclectically empty.

- "A Modern Theorist's Vindication of Adam Smith", The American Economic Review, Vol. 67, No. 1, Papers and Proceedings of the Eighty-ninth Annual Meeting of the American Economic Assocation (Feb., 1977)

- The small investor can now, for the first time, invest in common stocks and bonds in an efficient and convenient way. I am talking about people who don't have $ 10 million; who don't want to take unnecessary gambles; who operate under no Napoleonic delusions of being able to pick winners that will quadruple their money; who begrudge every minute devoted to keeping tax and personal records, and wish to think about their investments only at New Year's and when preparing their tax returns. Disinterested experts in finance prescribe for such people as follows: 1. Depending on your tolerance for the irreducible risks involved in owning common stocks, decide what portion of your nest egg you wish to keep in common stocks: 0, 100, 30 or 70 per cent. No one can decide this for you. You must decide at what point you'll sleep best at night, and whether eventually stocks will provide a better inflation hedge than they have done these last dozen years. ( Many will settle for 50-50. ) 2. For what common stocks you do decide to own, follow the golden rules of prudence : Diversify broadly, hold down costly turnover, keep all fees (and book- keeping !) minimal. 3. The same rules (diversification, etc.) apply to your holdings of tax-free and ordinary bonds. If you have taxable income of $ 20,000 or more, probably the bulk of your bonds should be " municipals " -i.e., state and local issues that escape all Federal tax because Congress refuses to close this loophole. Less affluent people will probably do as well in local savings accounts as in anything else. Now you know what to do. How do you do it?

- "Coping Sensibly," Newsweek (6 March 1978)

- The recent market run-up that appreciated run-of-the-mill shares also chanced to send up those token gold holdings. Pure luck, undeserved and unlikely to reoccur. Good questions outrank easy answers.

- "Gold and Common Stocks", Newsweek (21 August 1978)

1980s

[edit]- Mathematics is the handmaiden of the sciences. But mathematics also has a life of her own, gaining as much in her own development and fulfillment from the sciences as she gives to them. To help describe how apples and planets fall, and how ropes hang, Newton and Leibniz developed the calculus. By serendipity, that mode of analysis permitted economists to perfect the theory of general equilibrium two centuries later.

- Foreword to Theory of Technical Change and Economic Invariance: Application to Lie Groups, by Ryuzo Sato (1981)

- Yes, Keynes was a genius. Yes, some of his ideas were inchoate and would not have lent themselves usefully to diagramming and symbolic manipulation. Yes, by the time of the Radcliffe committee many of his British admirers were still frozen in the Model T version of his system. And yes, Keynes resented excessive simplifying of his paradigms.

Nevertheless, in science it is not the incoherent, inchoate and ineffable that has a cash value. If that were so, Goethe would be a greater scientist than either Einstein or Newton. What matters is the Kuhnian paradigm that people who are not geniuses can use. That which so many scholars independently agreed upon cannot be independent of the text that Keynes wrote down for them to read. What is remarkable is not the cogency of the case that Leijonhufvud manages to muster, which is rather flimsy, but rather how strong was the latent demand in the 1970s for a work to debunk Keynesianism. Harry Johnson put the same point in a different way.- "The Keynes Centenary: Sympathy from the other Cambridge", The Economist Vol. 287 (1983),; later in The Collected Scientific Papers of Paul Samuelson, Volume 5 (1986), p. 277-278

- An optimist who lived at a time when the world economy was running so badly that clever gimmicks could still work wonders, Keynes's object was to save capitalism from itself. In the end, his prescription in its most simple form self-destructed, as the obligation to run a full-employment humanitarian state caused modern economies to succumb to the new disease of stagflation - high inflation along with joblessness and excess capacity.

Economists of the most diverse views are constantly asking themselves: What would Keynes advise if he were now alive. And usually - whether the economist is a free-marketeer like Friederick von Hayek or one with strong interventionist leanings like John Kenneth Galbraith - they pay Keynes the supreme compliment of believing that if brought back to earth, Maynard would be favoring just what each of them happens to favor.

One also might wonder what Lord Keynes would prescribe for the huge structural deficit of Ronald Reagan, with the crowding out of investment that it implies once the American economy reattains high levels of employment.- "The House That Keynes Built", The New York Times (May 29, 1983)

- After 1929 it was the sturdy middle classes, and not just the lumpen proletariat, who were down and out. It was not all that unfashionable or disreputable to be bankrupt. By the last Hoover years, the states and localities had run out of money for relief. In middle-class neighborhoods like mine, you constantly had children at the door, asking by mouth or with a note for a dime, a quarter, or a potato: saying, in a believable fashion, we are starving.

- "Succumbing to Keynesianism", Challenge (1985)

- I can claim that in talking about modern economics I am talking about me. My finger has been in every pie. I once claimed to be the last generalist in economics, writing about and teaching such diverse subjects as international trade and econometrics, economic theory and business cycles, demography and labor economics, finance and monopolistic competition, history of doctrines and locational economics.

- February 1985, in William Breit and Roger W. Spencer (ed.) Lives of the laureates (5th ed., 2009)

- I reproach myself for a gross error. But I would reproach myself more if I had persisted in an error after observations revealed it clearly to be that. I made a deal of money in the late 1940s on the bull side, ignoring Satchel Paige’s advice to Lot’s wife, “Never look back.” Rather I would advocate Samuelson’s Law: “Always look back. You may learn something from your residuals. Usually one’s forecasts are not so good as one remembers them; the difference may be instructive.” The dictum “If you must forecast, forecast often,” is neither a joke nor a confession of impotence. It is a recognition of the primacy of brute fact over pretty theory. That part of the future that cannot be related to the present’s past is precisely what science cannot hope to capture. Fortunately, there is plenty of work for science to do, plenty of scientific tasks not yet done.

- February 1985, in William Breit and Roger W. Spencer (ed.) Lives of the laureates (5th ed., 2009)

- My mind is ever toying with economic ideas and relationships. Great novelists and poets have reported occasional abandonment by their muse. The well runs dry, permanently or on occasion. Mine has been a better luck. As I have written elsewhere, there is a vast inventory of topics and problems floating in the back of my mind. More perhaps than I shall ever have occasion to write up for publication. A result that I notice in statistical mechanics may someday help resolve a problem in finance.

- February 1985, in William Breit and Roger W. Spencer (ed.) Lives of the laureates (5th ed., 2009)

- The museums of science are replete with fossils of species that could not last the course. The leading-coinciding-lagging indicators might be buried forever in old footnotes. But occasionally Sleeping Beauty is brought back to life by the kiss of a new Prince Charming.

- "Paradise Lost & Refound: The Harvard ABC Barometers", The Journal of Portfolio Management, 13(3), 4-9, 1987

- What is truly discouraging — or reassuring? — is the considerable evidence that the universe of those who seek to be "timers," and vary the fractional shares of their portfolios committed to common stocks in the hope of enlarging average long-term total return, in fact fail to achieve on the average any plus gain in comparison with simply buying and holding a fixed fraction of common stocks.

- "Paradise Lost & Refound: The Harvard ABC Barometers", The Journal of Portfolio Management, 13(3), 4-9, 1987

- The goals, methods, and strategies of what borders on science is different from the gyration of fashion and the incommensurability of arts and music in different epochs. Because this different process of cumulative science is imperfect, historians and philosophers of science intermittently downplay this difference.

- "Keeping Whig History Honest", History of Economics Society Bulletin, 10(2), 161-167, 1988.

- The moral I take to be this. The virtues of alternative modern paradigms in science have to be evaluated in modern times and with modern methods. Until one schemata comes to dominate the other, Whig Historians will have interest in a diversified portfolio of archeological researches. As one paradigm loses out in the Darwinian jungle of science, what survives competitively in the agenda for dogmengeschicte cannot help but be altered.

- "Keeping Whig History Honest", History of Economics Society Bulletin, 10(2), 161-167, 1988.

1990s

[edit]- Let us summarise the lessons learned.

1. Though achieving private-property perfect competition will achieve productive efficiency, moving toward it may have made matters worse. And, in the land-enclosure problem, the transition must make things worse before they get better when lands are virtually homogeneous.

2. In the realistic case where lands differ in quality, partial privatisation may also worsen efficiency - even though ultimately efficiency will be enhanced by the deregulation process.

3. However, in the realistic case, an optimal choice of lands to be first privatised could be first to improve the commons. The rule for a 'perfectly-discriminating deregulator' to follow is evidently this: privatise those lands first whose 'imputed labour share'- as measured by the MP/AP fraction- is the lowest. That way, the first bit of deregulation can do more good than harm, as labour is transferred away from low marginal-product locations; that way, if there is inevitable transition harm, it can be kept to a minimum. There would seem to be a presumption that things get worse before they get better in such a programme of moving toward laissez-faire.- "When Deregulation Makes Things Worse Before They Get Better" in C. Moir and J. Dawson (eds.), Competition and Markets, Essays in Honour of Margaret Hall (1990)

- There were many Moliére characters speaking Keynesian prose in the depression years before 1936. What Keynes’s General Theory gave us, which Ohlin’s inspired journalisms could not at all offer, was a new manageable paradigm that we could explicitly express — and test, and criticize, and improve, ... , and be bewitched by.

Long before Kuhn, Schumpeter used to insist that old theories are not killed by simple facts: It takes a new theory to kill an old one. The mind cannot operate in terms of a melange of sensations. It needs a road map to perceive patterns of regularity and persistence.- "Thoughts on the Stockholm School and on Scandinavian Economics" in L. Jonung (ed.), The Stockholm School of Economics Revisited (1991)

- As a theorist I have great advantages. All I need is a pencil (now a ball pen) and an empty pad of paper. There are analysts who sit and look vacantly out the window, but after the age of 20 I was not one of them. I ought to envy the new generation who have grown up with the computer, but I don’t. None of them known to me sits idly at the console, improvising and experimenting in the way that a composer does at the piano. That ought to become increasingly possible. But up to now, in my observation, the computer is largely a black box into which researchers feed raw input and out of from which they draw various summarizing measures and simulations. Not having access to look around in the box, the investigator has less intuitive familiarity with the data than used to be the case in the bad old days.

- “My Life Philosophy: Policy Credos and Working Ways,” in M. Szenberg (ed.) Eminent Economists: Their Life Philosophies (1992)

- It is some relief to move from the exalted realm of philosophical ethics to the mundane realm of scientific methodology. However, I rather shy away from discussions of Methodology with a capital M. To paraphrase Shaw: Those who can do science; those who can’t prattle about its methodology.

- “My Life Philosophy: Policy Credos and Working Ways,” in M. Szenberg (ed.) Eminent Economists: Their Life Philosophies (1992)

- A scientist earns the only mortality worth having. Of the good scholar we say: Rex numquam moritur.

- Foreword to H. Herberg and N. Van Long (eds.) Trade, Welfare, and Economic Policies, Essays in Honor of Murray C. Kemp (1993)

- I will not waste ink on face-saving tautologies. When the governess of infants caught in a burning building reenters it unobserved in a hopeless mission of rescue, casuists may argue; "She did it only to get the good feeling of doing it. Because otherwise she wouldn't have done it." Such argumentation (in Wolfgang Pauli's scathing phrase) is not even wrong. It is just boring, irrelevant, and in the technical sense of old-fashioned logical positivism "meaningless."

- "Altruism as a Problem Involving Group versus Individual Selection in Economics and Biology", American Economic Review, 83(2) 143-148, 1993

- Orthodox biologists are like orthodox economists. When confronted by tensions between their paradigms and reality, they work to explain away the aberrations.

- "Altruism as a Problem Involving Group versus Individual Selection in Economics and Biology", American Economic Review, 83(2) 143-148, 1993

- Darwin's evolution is indeed mere sound and fury, signifying nothing normative, rather than denoting a process of meaningful Spencerian triumph. Natural selection is not an empty tautology about survival of those who survive. It is a lawful process subject to shrewd predictions and testable refutations. But in general it does not act to maximize any scalar magnitude. Many of its subprocesses do eschew submaximal configurations, and some may approximate efficiency criteria, but the resultant of them all is only positivistic!

- "Altruism as a Problem Involving Group versus Individual Selection in Economics and Biology", American Economic Review, 83(2) 143-148, 1993

- Social Darwinism is a perverted borrowing from what can be validly established for biology. When I contemplate strong claims by a Richard Posner that law has evolved historically a la Pareto, or arguments that a Coase Theorem ensures that deadweight loss is at its feasible minimum, I fear that von Neumann and Morgenstern are spinning in their graves and Charles Darwin is wondering why he left his barnacles, pigeons, and earthworms.

An unsupported claim by an economist- Darwinist does not acquire validity from a cited analogy with evolution. Truth must find its own legs to stand on.- "Altruism as a Problem Involving Group versus Individual Selection in Economics and Biology", American Economic Review, 83(2) 143-148, 1993

- Error is a virus that tends to spread. As I have already hinted, the categories of circulating capital and of the wage fund tended and still tend to get confounded together.

- "The Classical Classical Fallacy", Journal of Economic Literature, 32(2), 620-639, 1994.

- To the student of economic history the preponderant truth is that technical change has since 1750 tended to raise market clearing real wage rates. This property of the Age After Newton is hard to understand and explicate if you believe that sterile congealed-dead-labor is embodied in machines almost infinitely substitutable for live labor; equally confusing to you will be the truth that inventions which are labor saving may at the same time be wage raising! The doctrines of equated rates of surplus value moved Marxians backward from square one in the understanding of the laws of motion of the capitalistic system or the system of the Mixed Economy.

- "The Classical Classical Fallacy", Journal of Economic Literature, 32(2), 620-639, 1994.

- Economics, even classical economics, is not a finished business. There are still issues relevant to the present debate that have not been definitively explored.

- "The Classical Classical Fallacy", Journal of Economic Literature, 32(2), 620-639, 1994.

- The Coase-Samuelson generation were brought up witnessing the great debate between von Mises and Lerner-Lange concerning the feasibility of socialist rational pricing to produce Utopia. (That was a reprise of earlier Pareto-Barone-Wieser-Taylor debates.) Many contemporaries believed Lerner-Lange triumphed in the debate. I came to believe that Friedrich Hayek was the true victor.

Under static conditions where all is known or knowable (to whom?), whatever optimal states laissez-faire might occasion, so could some computer solution or some algorithms of play the game of competition also achieve. But in the real world all is changing, even in the time it takes me to write this sentence. Hayek has been persuasive — not in Whig ideology or in declaring that moderate reform of laissez-faire leads inevitably down the road to totalitarian socialism but — in arguing that experience suggests that only with heavy dependence on market pricing mechanisms can there be realized quasi-efficient and quasi-progressive organization of societies involving humans as Darwinian history has equeathed them. If a reader does not find the Hayek dynamic arguments persuasive, I will not here argue the matter further.- "Some uneasiness with the Coase Theorem", Japan and the World Economy 7 (1995)

- The vogue of vulgar and vague Coaseism, one hypothesizes, is strongest among libertarians and other devotees of laissez-faire who believe to find in it ammunition against regulation and voters' activism. Whether this hypothesis is close to or wide off the mark is of no importance. What does matter is how much deadweight-loss obtains in real life.

- "Some uneasiness with the Coase Theorem", Japan and the World Economy 7 (1995)

- What sex is to the biology classroom, stocks and investment riskiness is to the sophomore economics lecture hall.

- "Samuelson's Economics at Fifty: Remarks on the Occasion of the Anniversary of Publication" (1998)

- I tell no secret when I repeat that fame and reputation are much a matter of luck and chance.

- "Samuelson's Economics at Fifty: Remarks on the Occasion of the Anniversary of Publication" (1998)

- The pre-1800 pattern of commercial panics had to be a case of NON MACRO-EFFICIENCY of markets. We’ve come a long way, baby, in two hundred years toward micro efficiency of markets: Black-Scholes option pricing, indexing of portfolio diversification, and so forth. But there is no persuasive evidence, either from economic history or avant garde theorizing, that MACRO MARKET INEFFICIENCY is trending toward extinction: The future can well witness the oldest business cycle mechanism, the South Sea Bubble, and that kind of thing. We have no theory of the putative duration of a bubble. It can always go as long again as it has already gone. You cannot make money on correcting macro inefficiencies in the price level of the stock market.

- "Summing Up On Business Cycles: Opening Address" in Jeffrey C. Fuhrer, Scott Schuh (eds), Beyond Shocks: What Causes Business Cycles? (1998)

- Most of mainstream economics is not "big-picture economics." Our journals and textbooks are full of the grimy details about inventory cycles or the deadweight losses incident to taxes and regulation. Besides, most big pictures are wrong.

- "Two Gods That Fail", Challenge, 42(5), 29-33, 1999.

- Years ago Arthur Koestler edited The God That Failed, whose chapters report the disillusionment of one true believer after another in the promise of Marxian prophecies under the impact of contemporary actuality. It would be boring sawing of saw dust to elaborate on that god that failed. More relevant to the present moment of global economic chaos is an antipodal-polar archetype. I am speaking about the god of pure libertarian capitalism.

- "Two Gods That Fail", Challenge, 42(5), 29-33, 1999.

2000s

[edit]- Years ago, I wrote aphoristically: “Inside a classical economist, you discern a neoclassical economist trying to get in.” My archetypical tableaux flesh out this heuristic perception. And, in my considered opinion, these explications cast cogent doubts on that view popular in the 1950s and early 1960s that “going back to the classics” somehow offered a different and better alternative to the post-neoclassical mainstream paradigms.

- "A Quintessential (ahistorical) Tableau Economique: To Sum up Pre- and Post-Smith Classical Paradigms" in J. Biddle, J. Davis and S. Medema (eds.), Economics Broadly Considered, Essays in Honour of Warren Samuels (2001)

- An economy’s inventory of produced inputs is both complex and simple. Maintaining and improving upon congeries of productive inputs is an indispensable part of economic progress. All such time-phased processes will not evolve automatically: cave-people rose and fell in material well-being; eons passed without much cumulative change; great diversity of performance characterized geographically separated societies. Attempts to generalize simple family’s or related-families’ habit formation to large-group polities—à la utopian experimental cults or in the Lenin-Stalin and Mao pattern have not hitherto succeeded in organizing production with approximate Pareto-Optimality efficiency features. Gradual evolution toward near laissez-faire market mechanism responding to individual’s self-interest, history suggests and advanced economic theory second guesses, will incur areas of market failure and will generate and perpetuate considerable degrees of economic and political inequalities. Just as there is no asymptotic communist utopia, neither is an asymptotic laissez-faire utopia.

- "A Modern Post-Mortem on Böhm's Capital Theory: Its Vital Normative Flaw Shared by Pre-Sraffian Mainstream Capital Theory", Journal of the History of Economic Thought, Volume 23, Number 3 (2001)

- Economics never was a dismal science. It should be a realistic science.

- quoted in K. Puttaswamaiah, "Contributions of Paul A. Samuelson", in K. Puttaswamaiah, Paul Samuelson and the Foundations of Modern Economics (2002)

- You must realize how bad, temporarily, capitalism had become in public opinion. I remember seeing a poll of small town attitudes in local newspapers. They asked questions like "should we nationalize the banking system?" More than half of those editors, about the most conservative group in the world, were in favor of nationalizing the banking system. Father Coughlin, the Detroit demagogue who turned anti-Semitic, complained about "fountain pen money, the perpetrator of great wealth, the money changers in the temple." It was kind of a crude expansionism. Huey Long and "every man a millionaire," or whatever it was. So I would say that Keynes thought of himself as saving the system. And lots of the New Dealers ― original New Dealers, Veblenites, technocrats ― did not like Keynesian economics. They said "that is using palliatives, it's not getting rid of the wicked capitalistic ethos." Keynes told Roosevelt when he came here in 1933 that he needed to spend so much more per month in deficit spending. He gave very precise figures with great self-confidence.

- Interview with Parker in Randall E. Parker (ed.), Reflections on the Great Depression (2002)

- Modigliani's theory was a powerful searchlight on what was happening... It is the best explanation of what has actually been happening in the great swing of American life since the 1950's.

- Paul Samuelson in: Louis Uchitelle. "Franco Modigliani, 85, Nobel-Winning Economist, Dies" in New York Times, September 26, 2003.

- However, one last caution. What has happened in Japan for 12 long years warns that an affluent society like America’s might not be immune to a self de-energization of its optimism and free spending. Do not bet on worst case scenarios. But do not ignore them completely either.

- "Tale of two macroeconomies", Japan and the World Economy 15 (2003)

- The proof of the pudding is in the eating. There was a widespread myth of the 1970s, a myth along Tom Kuhn’s (1962) Structure of Scientific Revolutions lines. The Keynesianism, which worked so well in Camelot and brought forth a long epoch of price-level stability with good Q growth and nearly full employment, gave way to a new and quite different macro view after 1966. A new paradigm, monistic monetarism, so the tale narrates, gave a better fit. And therefore King Keynes lost self esteem and public esteem. The King is dead. Long live King Milton!

Contemplate the true facts. Examine 10 prominent best forecasting models 1950 to 1980: Wharton, Townsend–Greenspan, Michigan Model, St. Louis Reserve Bank, Citibank Economic Department under Walter Wriston’s choice of Lief Olson, et cetera. … M did matter as for almost everyone. But never did M alone matter systemically, as post-1950 Friedman monetarism professed.- in William A. Barnett, An Interview with Paul A. Samuelson (December 23, 2003)

- A later writer, such as Leijonhufvud, I knew to have it wrong, when he later argued the merits of Keynes’s subtle intuitions and downplayed the various (identical!) mathematical versions of The General Theory. The so-called 1937 Hicks or later Hicks–Hansen IS–LM diagram will do as an example for the debate.

- in William A. Barnett, An Interview with Paul A. Samuelson (December 23, 2003)

- I would guess that most MIT Ph.D.’s since 1980 might deem themselves not to be “Keynesians.” But they, and modern economists everywhere, do use models like those of Samuelson, Modigliani, Solow, and Tobin. Professor Martin Feldstein, my Harvard neighbor, complained at the 350th Anniversary of Harvard that Keynesians had tried to poison his sophomore mind against saving. Tobin and I on the same panel took this amiss, since both of us since 1955 had been favoring a “neoclassical synthesis,” in which full employment with an austere fiscal budget would add to capital formation in preparation for a coming demographic turnaround.

- in William A. Barnett, An Interview with Paul A. Samuelson (December 23, 2003)

- Often I’ve stated how I hate to be wrong. That has aborted many a tempting error, but not all of them. But I hate much more to stay wrong. Early on, I’ve learned to check back on earlier proclamations. One can learn much from one’s own errors and precious little from one’s triumphs. By September of 1945, it was becoming obvious that oversaving was not going to cause a deep and lasting post-war recession. So then and there, I cut my losses on that bad earlier estimate.

- in William A. Barnett, An Interview with Paul A. Samuelson (December 23, 2003)

- My notion of a fruitful economic science would be that it can help us explain and understand the course of actual economic history. A scholar who seriously addresses commentary on contemporary monthly and yearly events is, in this view, practicing the study of history—history in its most contemporary time phasing.

- in William A. Barnett, An Interview with Paul A. Samuelson (December 23, 2003)

- Instead of attenuating this paper’s theses, heterogeneity amplifies its importance. Contemplate a scenario where Schumpeter’s fruitful capitalist destruction harms a really sizeable fraction of the future U.S. population and, say, improves welfare of another group and does that so much as to justify a calculation that the winners could be made to transfer some of their gains and thereby leave no substantial U.S. group net losers from free trade. Should noneconomists accept this as cogent rebuttal if there is no evidence that compensating fiscal transfers have been made or will be made? Marie Antoinette said, “Let them eat cake.” But history records no transfer of sugar and flour to her peasant subjects. Even the sage Dr. Greenspan sometimes sounds Antoinette-ish. The economists’ literature of the 1930s—Hicks, Lerner, Kaldor, Scitovsky and others, to say nothing of earlier writings by J.S. Mill, Edgeworth, Pareto and Viner—perpetrates something of a shell game in ethical debates about the conflict between efficiency and greater inequality.

Policy aside and ethical judgments aside, mainstream trade economists have insufficiently noticed the drastic change in mean U.S. incomes and in inequalities among different U.S. classes. As in any other society, perhaps a third of Americans are not highly educated and not energetic enough to qualify for skilled professional jobs. If mass immigration into the United States of similar workers to them had been permitted to actually take place, mainstream economists could not avoid predicting a substantial drop in wages of this native group while the new immigrants were earning a substantial rise over what their old-country real wages had been.- "Where Ricardo and Mill Rebut and Confirm Arguments of Mainstream Economists Supporting Globalization", Journal of Economic Perspectives (Summer 2004)

- An evolving discipline–whether it be history or economics or astrophysics or immunology–is ever dynamically changing. Two steps forward and X steps back, so to speak. Periodically, the scholarly group registers more or less self-confidence, self-esteem, and complacency. We careerists are happiest when recent past achievements have seemed to be successful, but when still there are completable tasks dimly visible ahead.

- "Foreword: Eavesdropping on the Future?" in New Frontiers in Economics (2004)

- Here is my advice. When in doubt, give my new efforts a hearing. Many feel a calling to break new ground; in the end, few will end upfinding their efforts chosen. But the yea-sayer does do less harm than the naysayer, in that the Darwinian process of adverse testing will in time (most likely?) separate the useful from the useless, the trivial from the profound.

- "Foreword: Eavesdropping on the Future?" in New Frontiers in Economics (2004)

- I had a great admiration for Pigou. I thought that, in many ways, he was not only a faithful follower of Alfred Marshall, but he was also a more fertile developer of the Marshallian tradition than Marshall himself. … Whitehead said to me:“Don’t you think that Pigou was an overrated economist? Wasn’t Foxwell a better man?” Since I am an honest man, I said to Whitehead:“No, I think Pigou was a much more important economist than Foxwell.”

- Kotaro Suzumura, An interview with Paul Samuelson: welfare economics,“old” and “new”, and social choice theory (2005)

- I think Marshall was a great economist, but he was a potentially much greater economist than he actually was. It was not that he was lazy, but his health was not good, and he worked in miniature.

- Kotaro Suzumura, An interview with Paul Samuelson: welfare economics,“old” and “new”, and social choice theory (2005)

- Arrow’s general impossibility theorem does not disprove the existence of the Bergsonian social welfare function, neither does it disprove the existence of the Benthamite hedonistic function.

- Kotaro Suzumura, An interview with Paul Samuelson: welfare economics,“old” and “new”, and social choice theory (2005)

- I return to economics and to economists, and to the question of why the profession’s directions have evolved in the manners evident from this book. A major conservative economist once explained that a source of his antipathy to government traced back to the defeat of his southern ancestors by a larger north economy. Here is a similar factoid. Joan Robinson once wrote that her opposition to having the U.K. enter the European Market was due to the fact that she “had more friends in [Nehru’s] India than on the continent.”

- Coeditor's Forword in Inside the economist’s mind: conversations with eminent economists (2007)

- We economists love to quote Keynes’s final lines in his 1936 General Theory—for the reason that they cater so well to our vanity and self-importance. But to admit the truth, madmen in authority can self generate their own frenzies without needing help from either defunct or avant-garde economists. What establishment economists brew up is as often what the Prince and the Public are already wanting to imbibe. We guys don’t stay in the best club by proffering the views of some past academic crank or academic sage.

- Coeditor's Forword in Inside the economist’s mind: conversations with eminent economists (2007)

- My final words are cut short by this audience’s well-fed drowsiness. I will leave as a question for later discussion: Will hedge funds make our golden years more golden, or will the new concoctions of option engineers, instead of reducing risks by spreading them optimally (in fact, by making possible about 100 to 1 over leveraging), result in microeconomic losses for pension funds and, maybe someday, even threaten the macro system with lethal financial implosions?

- "Is Personal Finance a Science?", in Z. Bodie, D. McLeavey and L.B. Siegel (eds.) The Future of Life-Cycle Saving and Investing (2007)

- What then is it that, since 2007, has caused Wall Street capitalism's own suicide? At the bottom of this worst financial mess in a century is this: Milton Friedman-Friedrich Hayek libertarian laissez-faire capitalism, permitted to run wild without regulation. This is the root source of today's travails. Both of these men are dead, but their poisoned legacies live on.

- "Farewell to Friedman-Hayek Libertarian Capitalism", Tribune Media Services (2008)

- Scholars still debate whether Columbus brought syphilis to the New World or vice versa. But it cannot be doubted that the 2008 world meltdown carries on its label the words Made in America.

- "Farewell to Friedman-Hayek Libertarian Capitalism", Tribune Media Services (2008)

- Well, I will say this. And this is the main thing to remember. Macroeconomics -- even with all of our computers and with all of our information -- is not an exact science and is incapable of being an exact science. It can be better or it can be worse, but there isn't guaranteed predictability in these matters.

- Conor Clarke, An Interview With Paul Samuelson, Part One (2009)

- Well, I'd say, and this is probably a change from what I would have said when I was younger: Have a very healthy respect for the study of economic history, because that's the raw material out of which any of your conjectures or testings will come. And I think the recent period has illustrated that. The governor of the Bank of England seems to have forgotten or not known that there was no bank insurance in England, so when Northern Rock got a run, he was surprised. Well, he shouldn't have been.

But history doesn't tell its own story. You've got to bring to it all the statistical testings that are possible. And we have a lot more information now than we used to.- Conor Clarke, An Interview With Paul Samuelson, Part Two (2009)

- When I once called myself a “Sunday painter” dabbling in stochastic finance, that was not meant to belittle finance theory as a branch of serious economic theory. Such a peculiar view was expressed again and again by the late Milton Friedman, a dizzy view that I still find incomprehensible.

- "An Enjoyable Life Puzzling Over Modern Finance Theory", Annu. Rev. Financ. Econ. 2009. 1:19–35

- From the beginning I could not believe that the “efficient market” hypothesis was dependent on a pure Brownian motion white noise or any truly random random walk. Place a minuscule colloidal molecule on a horizontal table that covers unlimited acres. Bombard it from every direction with thousands of minute atoms; and then if you wait long enough that original molecule can have traveled a billion miles in one direction. That’s truly a random Bachelier-Einstein walk, but not my notion of economic fluctuations.

- "An Enjoyable Life Puzzling Over Modern Finance Theory", Annu. Rev. Financ. Econ. 2009. 1:19–35

- Moral: To understand economics you need to know not only fundamentals but also its nuances. Darwin is in the nuances. When someone preaches “Economics in one lesson,” I advise: Go back for the second lesson.

- "An Enjoyable Life Puzzling Over Modern Finance Theory", Annu. Rev. Financ. Econ. 2009. 1:19–35

- Moral: free markets do not stabilize themselves. Zero regulating is vastly suboptimal to rational regulating. Libertarianism is its own worst enemy!

- "An Enjoyable Life Puzzling Over Modern Finance Theory", Annu. Rev. Financ. Econ. 2009. 1:19–35

- Markets are not perfect, which is true even for rationally regulated markets. Nevertheless, over the last thousand years every attempt to organize sizeable societies without important dependence on markets has generated its own failure ...

- "An Enjoyable Life Puzzling Over Modern Finance Theory", Annu. Rev. Financ. Econ. 2009. 1:19–35

Quotes about Paul Samuelson

[edit]- Paul Samuelson is omnipresent in American and even world economics; like Joyce's Humphrey Chimpeden Earwicker or Melville's Confidence Man,. he appears at every turn of history and in every disguise.

- Kenneth J. Arrow, "Samuelson Collected", Journal of Political Economy Vol. 75, No. 5 (Oct., 1967), pp. 730-737

- Paul’s work combined breadth and intensity. On the one hand, his structures were grounded in a very wide knowledge of the nature of mathematical systems used to describe natural phenomena. On the other, he studied individual questions in economics, sometimes at a very detailed level.

- Kenneth J. Arrow, Foreword in Samuelsonian economics and the twenty-first century edited by Michael Szenberg, Lall Ramrattan, Aron A.. Gottesman (2006)

- As an intellectual and economist, there were two Samuelsons. There was the mathematical savant who had learned his trade at the feet of Viner, Leontief, Schumpeter and, above all, Wilson. This work had raised him above most of his contemporaries, enabling him to speak with the authority of one of the leading economists of his generation. However, his more popular work was not just a distillation of his abstract theories; it rested not on complex mathematical arguments but involved careful data analysis and familiarity with the way that economic institutions worked. This was the Samuelson, mentored by Hansen during the Second World War, who wrote Economics and whose views were sought by the press and government.

- Roger Backhouse, "The people’s economist" (10 February, 2020)

- I got to know Paul Samuelson well during 2001-02 when I was a visiting professor at MIT. I would pause every now and then at his office to chit-chat about things. He was into his grey years by then and seemed a bit lonely. His interests were voracious — from the intricacies of science to the lives of people and he liked to chat.

My last proper conversation with him was on May 15, 2002. I was photocopying something at MIT, when he stopped and said that it was his birthday that day. The Harvard Club would open a special champagne for him and he asked me if my wife and I would come to the Harvard Club. For an economist, that’s the equivalent of Einstein asking a physicist to dinner. I, of course, said yes, expecting lots of people there. It turned out to be a dinner with Samuelson, his charming wife Richa and the two of us. It was one of the most memorable evenings of my life. We — truth be told, mainly he —talked about art, history and, of course, economics.- Kaushik Basu, "He left his imprint on every field of economics" (Dec 14, 2009)

- For virtually my entire career in finance—now more than 61 years—two of the greatest economists of the past century have played a major role in my understanding of the financial markets. One is John Maynard Keynes, the legendary British theorist and author. The other is Paul Samuelson, the prolific generator of ideas and the first American to win (in 1970) the Nobel Memorial Prize in the Economic Sciences.

- John Bogle, "The (Non) Lessons of History—and the (Real) Lessons of Return Sources and Investment Costs", Proceedings of the American Philosophical Society Vol. 158, No. 3 (SEPTEMBER 2014),

- The readers of this space know Paul Samuelson as a witty, informed and often acerbic commentator on current affairs, as a “liberal” supporter of the economic policies of the Kennedy and Johnson years, and as a critic of current Nixon economic policy.

Millions of college graduates know Paul Samuelson for his economics textbook, which has been the leading elementary text in the United States for two decades, has sold nearly 3 million copies, and is almost surely the best-selling book on economics ever published in the Western world.

Professional economists know Paul Samuelson as a mathematical economist who has ranged widely and deeply, who has helped to reshape and improve the theoretical foundations of our subject. This is the work for which this remarkably versatile man won the Nobel Prize. In the words of the announcement, the prize was awarded “for the scientific work through which he has developed static and dynamic economic theory and actively contributed to raising the level of analysis in economic science.”- Milton Friedman, "Paul Samuelson", Newsweek (9 November 1970)

- Reference to the textbook and its writer was often made with a lofty sense of intellectual and literacy superiority; that has not been true in modern times in economics. The dominant influence, now fully respected, is that of Paul Samuelson. He is celebrated for his research, for his public advocacy, his stand for socially acceptable economic policy. He has not been sufficiently celebrated for this really phenomenal achievement: the basic economic education of successive generations. There are few Americans of any public distinction who do not owe some of their knowledge and position to Samuelson, and his influence is by no means confined to the United States. In ultimate teaching effect in economics, he has no rival

- John Kenneth Galbraith, "Paul Samuelson on His 90th Birthday", The American Economist (2007)

- Another big influence was Samuelson's Foundations, which I read when I stated here at Chicago. It's a "how-to-do-it" book. a great book for first-year graduate students. It says, "Here's the way you do it." It lets you in on the secret of how you play the game, as opposed to cutting you off with big words. I think the combination of Samuelson's book plays Friedman's class was what got me going.

- Robert E. Lucas, in Conversations with Economists (1983) by Arjo Klamer

- The only way I feel I understand something is if I can write it down in a model and make it work. I felt that from the beginning. That's why I liked Samuelson's book. He'll take these incomprehensible verbal debates that go on and on and never end and just end them; formulate the issue in such a way that the question is answerable, and then get the answer.

- Robert E. Lucas, in Conversations with Economists (1983) by Arjo Klamer

- Samuelson says I was wrong and he was right, and he froths at the mouth when people talk about the lighthouse example. He says Coase is wrong; he doesn't overcome the free rider problem. Who are the free riders? The foreign ships going past the British coast which do not call at a British port. Using Samuelson's approach, what do you do? Do you ask the foreign governments to give you a subsidy? Do you tax people in Britain because the foreign ships are getting help without paying for it? What do you do?

My approach is to compare the alternatives. People like Samuelson like to set up a perfect world and say that the market does not bring us to this point and imply that the government should do something. They stop their analysis at that point.- Ronald Coase, in "Looking For Results" (1997)

- Between meals I arranged a light, informal trivia competition. Had answers been counted, he would have won hands down. He even knew the third president—of Finland—a question I threw in as a joke.

- Bengt Holmstrom, quoted in Michael Szenberg, Lall Ramrattan and Aron Gottesman, "Ten Ways to Know Paul A. Samuelson" (2006)

- Generally speaking, Samuelson's contribution has been that, more than any other contemporary economist, he has contributed to raising the general analytical and methodological level in economic science. He has in fact simply rewritten considerable parts of economic theory. He has also shown the fundamental unity of both the problems and analytical techniques in economics, partly by a systematic application of the methodology of maximization for a broad set of problems. This means that Samuelson's contributions range over a large number of different fields.

- Award Ceremony Speech 1970 at nobelprize.org, by Professor Assar Lindbeck, Stockholm School of Economics.

- Of course, one can go back to high school or, in my case, junior college and find roots; there are some indeed, but my professional beginnings were in the Berkeley that existed just before World War II and the scholarship I won to MIT. There I met the dazzling wunderkind Paul Samuelson. When I was browsing in the Berkeley library and came across early issues of Econometrica, Samuelson’s contributions caught my eye. When I got an opportunity to go to MIT, it was the possibility of working with Samuelson that confirmed all my choices. I was attached to him as a graduate assistant from the outset, and I tried to maximize my contact with him, picking up insights that he scattered on every encounter.

Working with Samuelson, who was at the forefront of interpreting Keynesian theory for teaching and policy application, I was put immediately in the midst of two challenging contests—one to gain acceptance for a way of thinking about macroeconomics and another to gain acceptance for a methodology in economics, namely, the mathematical method. Later, both challenges were to be overcome, but for ten or twenty years opposition was fierce.

Once Samuelson’s Economics became a widely used text in first courses in the subject, Keynesian economics was firmly embedded. There was no turning back from that achievement. The successive student generations turned more toward the mathematical approach in graduate school, and they taught or did research in this vein. That eventually established the mathematical method, first in the United States, then in Europe, Japan, India, and other centers. Much of the foundation was built in Europe, and many of the American masters at mathematical economics were immigrants, but Samuelson, Friedman, and others gave it a native-born American flavor, and the approach truly caught on in this country.- Lawrence R. Klein, Lecture at Trinity University in October 1984, published in Lives of the Laureates (5th ed., 2009), edited by William Breit and Barry T. Hirsh,

- He knows history. If he had a Hungarian sitting at his side at the dinner table, he would quote easily names of politicians or novelists of the Austrian–Hungarian empire of the late 19th century. He also understands the significance of the history of a country. This is a rare quality at a time when the education of economists has become excessively technical.

- János Kornai, quoted in Michael Szenberg, Lall Ramrattan and Aron Gottesman, "Ten Ways to Know Paul A. Samuelson" (2006)

- [Paul] mentioned that he had heard about a piece I had written on Irving Fisher. I have no idea how he heard about it, but I offered to send him a copy and within a few days I got back a letter. [Paul] read the paper and wanted to set down his own interpretation, but then he closes the letter with a remarkable line that I treasure: ‘Do disregard my heresies and follow your own star.’

- Perry Mehrling, quoted in Michael Szenberg, Lall Ramrattan and Aron Gottesman, "Ten Ways to Know Paul A. Samuelson" (2006)

- In the world of music, it is a rarity to find a person who is both a gifted composer and a top conductor. So it is in economics as well. Paul is that rarity. When Paul is writing, the sun is always out. His writing—ever eloquent, ever stirring—is done with the kind of verve that one seldom finds today.

- Michael Szenberg, Lall Ramrattan and Aron Gottesman, "Ten Ways to Know Paul A. Samuelson" (2006)

- In contrast to the natural sciences, where Isaac Newton and Albert Einstein made their major contributions, most economics masterpieces were written when the authors were middle aged. Adam Smith, Karl Marx, John Maynard Keynes, and Milton Friedman come to mind. However, Paul started much earlier, in his 20s; and, even now, his new articles influence the fields of economics and finance.

- Michael Szenberg, Lall Ramrattan and Aron Gottesman, "Ten Ways to Know Paul A. Samuelson" (2006)

- Samuelson is an artist; he brought undergraduates pretty well up to the level of the state of knowledge in the profession.

- Edward C. Prescott, interview in Brian Snowdon and Howard R. Vane. Modern macroeconomics: its origins, development and current state. (2005)

- There have been hedgehogs; there have been foxes; and then there was Paul Samuelson. (...) I’m referring, of course, to Isaiah Berlin’s famous distinction among thinkers – foxes who know many things, and hedgehogs who know one big thing. What distinguished Paul Samuelson as an economic thinker, making him like nobody else, past or present, was the fact that he knew – and taught us – many big things. No economist has ever had so many seminal ideas.

- One recent history of economic thought (Jürg Niehans’s A History of Economic Theory) devotes twenty-four pages to Samuelson’s ideas. Adam Smith only gets thirteen. Samuelson’s work on stock markets and the random walk takes up less than two of those twenty-four pages. He was “the last generalist in economics,” as he liked to say, and for him financial market studies were just a side project that he at times seemed deeply ambivalent about. His intervention was, however, crucial to the triumph of the random walk. Here was one of the most important economists of all time, and he didn’t think the relationship between coin flips and the stock market was a dinner-speech triviality.

- Justin Fox, Myth of Rational Market (2009), Ch. 4 : A Random Walk from Paul Samuelson to Paul Samuelson

- A few years ago, I had the good fortune of running across a first edition of Paul's textbook (not the recent reprint of the original text, but an actual 1948 edition). It was a real find. I bought the volume in an online auction for, if my recollection is correct, $35. Talk about consumer surplus! I would have gladly paid many times that.

At the next Boston Fed meeting, I took the book along to get Paul to sign it. Below is the book's title page, along with Paul's gracious inscription.- Greg Mankiw, "Memories of Paul" (December 15, 2009)

- John Maynard Keynes may have had more influence on policy makers, Milton Friedman on citizens, Kenneth Arrow on economic theory, but Samuelson had more influence on the way economics is done today, and the purposes to which it is put, than any other economist of the twentieth century.

- David Warsh, "The Enormous Black Box" (2009)

- He was influential. He influenced students through his textbook, and he influenced the entire economics profession through his dissertation, published as "Foundations of Economic Analysis." Readers of this blog will tend to disapprove of his influence, in that it promoted Keynes and the use of mathematical modeling. Perhaps Milton Friedman was more influential on policy. But Samuelson was more influential on the internal dynamics of the economics profession. On that score, I would say that he was without peer in this century. […] Compared with later generations of economists, he was more nuanced in his thinking and not as capable a mathematician.

- Arnold Kling, Thoughts on the Late Paul Samuelson (2009)

- Many principles of economics were hidden in obscure verbiage of previous generations; he reformulated and extended them with crystal clarity in the language of mathematics.

- Avinash Dixit, "Paul Samuelson's Legacy" (2012)

External links

[edit]- "Paul A. Samuelson (Ideological Profiles of the Economics Laureates)," by Daniel B. Klein, and Ryan Daza. Econ Journal Watch 10.3 (2013): 561-569.

Categories:

- Academics from the United States

- Economists from the United States

- Nobel laureates in Economics

- Jews from the United States

- 1915 births

- 2009 deaths

- People from Gary

- Nobel laureates from the United States

- National Medal of Science laureates

- Harvard University alumni

- Massachusetts Institute of Technology faculty

- Fellows of the British Academy

- University of Chicago alumni